My soap-box rant

Why this rant?

Only 10% of Australians trust financial advisors. AFR 5/5/2014. A scary figure.

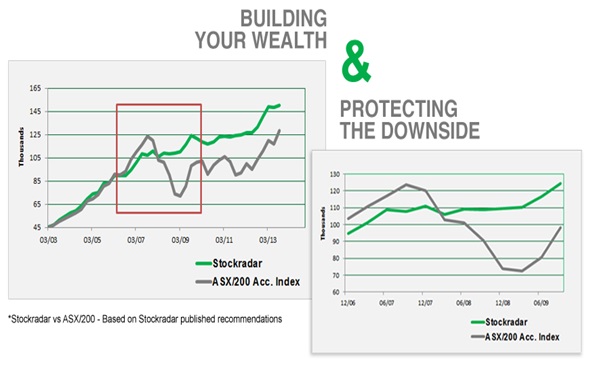

The “trust busting” GFC took a heavy toll on the financial advice industry. Most advisors floundered without a sound strategy for protecting your capital.

We wear our hearts on our sleeve at Stockradar. We are transparent with nothing to hide. We are independent with no products to push. Honesty, professionalism and our member’s fortunes are our passion. Our results are envied with special attention going to the ‘GFC’ period. Protect your wealth. Be prepared for the bull or the bear by having a sound and methodical strategy to guide you.